" When you consider ARMs versus repaired rates, it provides you a lot more flexibility." If you recognize how they function, these finances can be extremely advantageous. If you can afford it, any kind of extra payment goes directly toward the principle.

- The couple had actually been outbid on the very first house they tried to buy and really did not wish to take the chance of losing out once more.

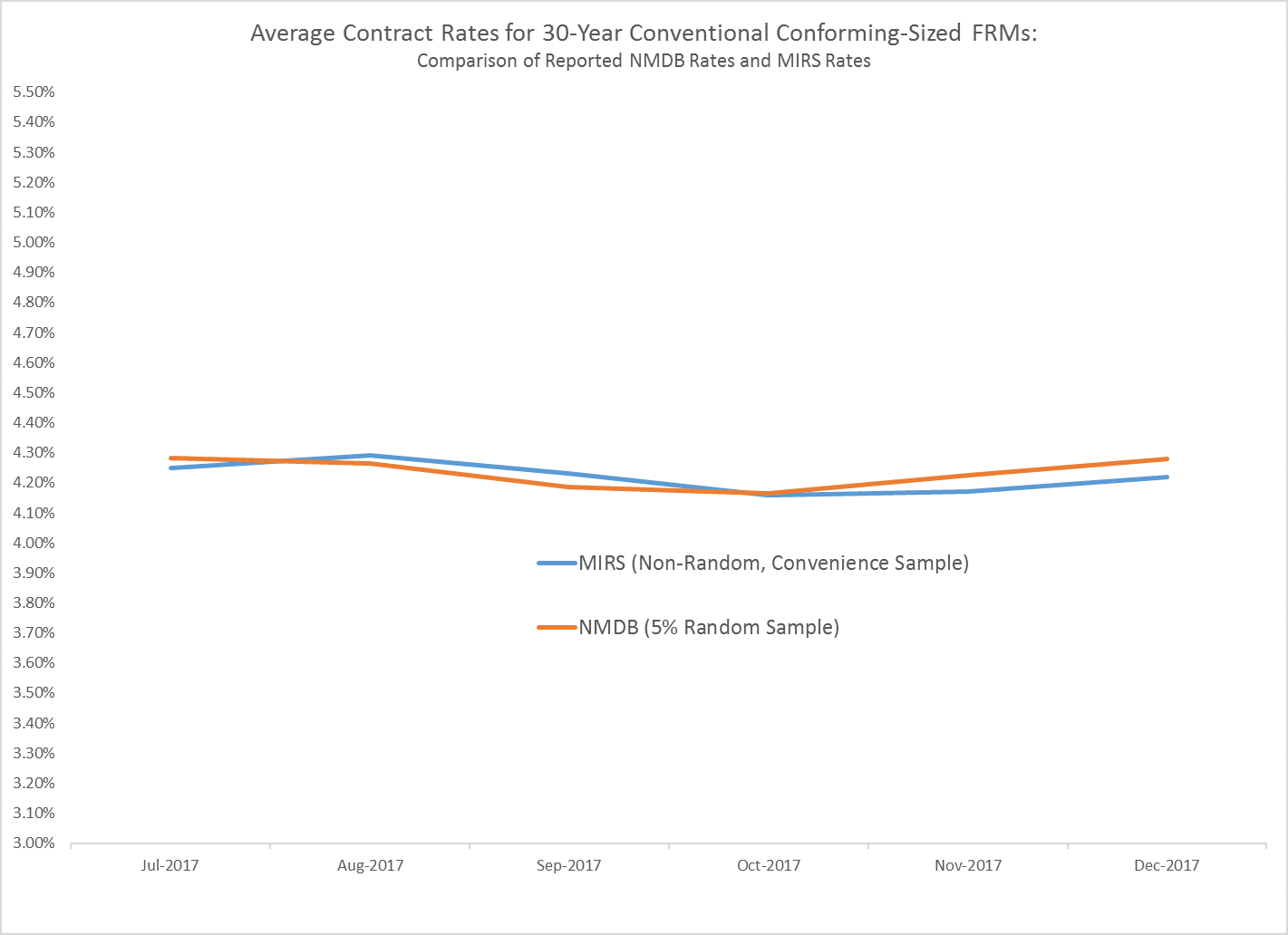

- " The impressive surge in home costs has people seeking to conserve money on regular monthly payments anywhere they can," states Matt Graham, principal of operations at the market publication Home loan News Daily.

- " I think there is still a need to use the product which is going to obtain you right into the residence and after that maybe there might be a chance to refinance into a fixed-rate home loan later on," Fratantoni told MarketWatch.

- A 5-1 ARM is a lending where the price is dealt with for 5 years, after that resets annually after that; a 7-1 ARM is a set rate for the very first seven years and so forth.

According to the Customer Financial Security Board, home mortgage servicers are required to send you a price quote of your new payment. If the ARM is resetting for the very first time, that price quote ought to be sent out to you seven to 8 months prior to the adjustment. If the loan has readjusted in the past, you'll be informed two to 4 months beforehand. The biggest advantage of an ARM is that it is substantially less costly than a fixed-rate home mortgage, at least for the initial 3, 5, or seven years. Although the rate of interest is dealt with, the total amount of rate of interest you'll pay depends upon the home mortgage term. Typical loan provider supply fixed-rate mortgages for a variety of terms, one of the most typical of which are 30, 20, and 15 years.

Just How Does Mortgage Passion Work?

If you want an ARM, there are a number of different setups to choose from. The basis on an ARM's price is the benchmark it names in the agreement. Treasury or the safeguarded over night money price as a price benchmark.

Whats The Difference Between Arms As Well As Standard Home Loans?

Financial institutions produced variable-rate mortgages to make monthly payments lower. Many individuals like the low, teaser rates offered by ARMs and assume they will run out the house before the flexible price duration takes https://6317373809e50.site123.me/#section-63173831533e5 control of and higher monthly repayments come due. Adjustable price home loans are commonly, but not always, more economical than fixed-rate mortgages.

Research Your Options

A lifetime cap is a limit on the amount that passion can raise over the life of the loan. So, as an example, if there is a 6% life time cap and also you have a 20-year ARM as well as the rate of interest has actually gone up 6% in the 10th year, it can not can you cancel timeshare purchase go any kind of greater, despite what else occurs. Your lender likewise identifies the margin you will certainly pay, which is the number of percent points added to index. The margin percent differs from one lending institution to the following and also must be defaulting on timeshares a prime focus of your study when getting an ARM.

Understand, though, that the longer the set period for your ARM, the higher the interest rate. If you're establishing on your own in a profession, if you're solitary as well as/ or childless, or if you simply have a short attention span, an ARM with the lowest price-- the 3/1 or 5/1-- possibly makes a great deal of feeling. You'll conserve a lot of money in interest while you have your residence, and also you're likely to be lengthy passed the time the lending starts adjusting. Take into consideration likewise that this was not long after the housing crisis, when homeowners discovered they couldn't rely on being able to market their residences within a few years of purchasing. That is, while the reduced, introductory rate for the ARM mortgage was still essentially.

If we placed that monthly savings on the principal, that's $4,255.80 much less on the balance at the end of the first 5 years. That implies that rather than your payment being $1,377.05 when the rates of interest resets at 5.5%, it would certainly be $1,350.91, as well as the passion savings over the life time of the loan. A 5/1 ARM is a sort of adjustable price home loan with a fixed rates of interest for the initial 5 years. Afterward, the 5/1 ARM switches to an adjustable rate of interest for the rest of its term. Adapting ARMs have life time price caps that offer borrowers some predictability.